For Ontario homeowners 55+

Building a retirement that actually works for you

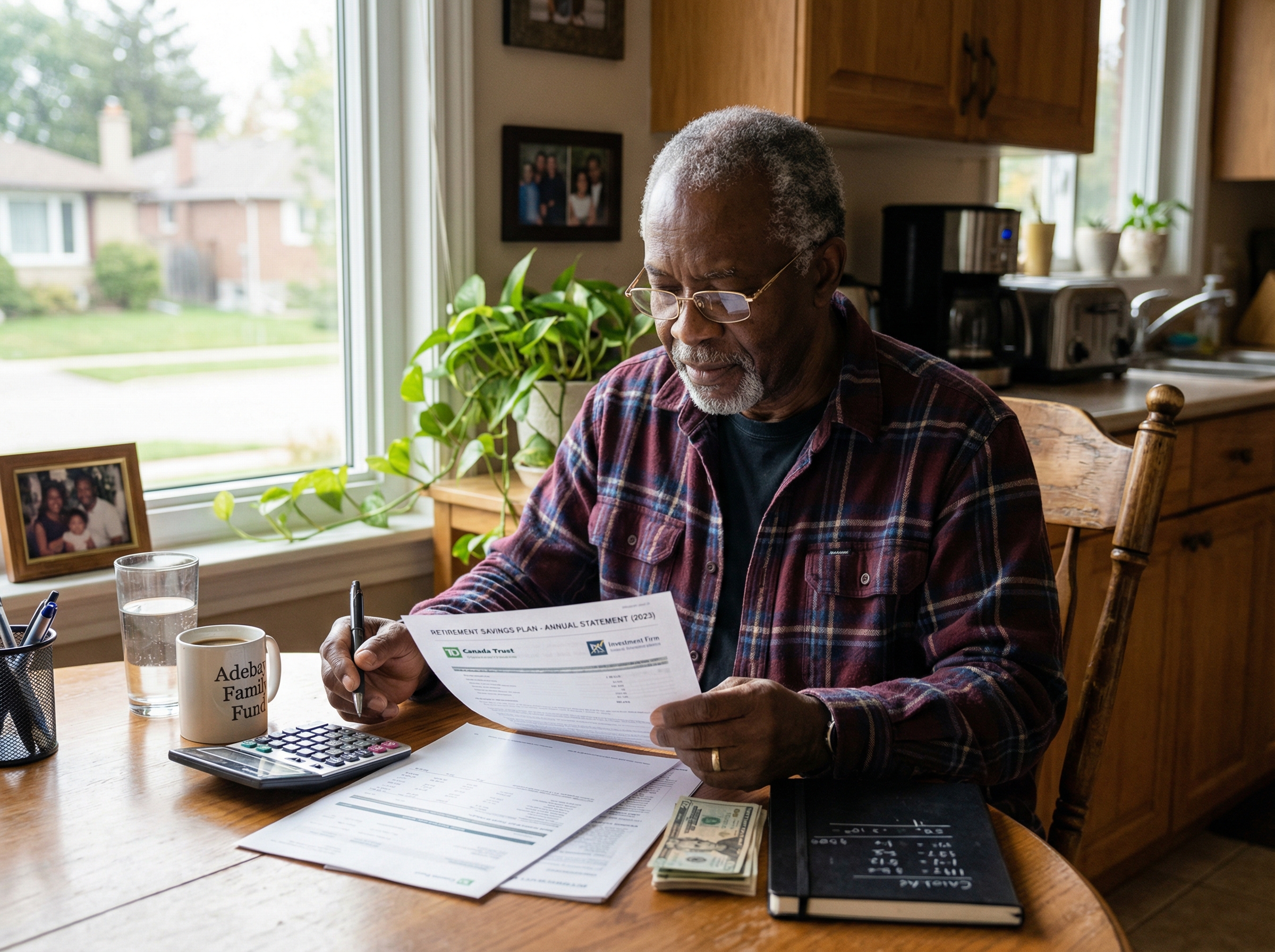

Retirement planning gets talked about like it's one big decision. It isn't. It's a dozen small ones — what benefits you're owed, what your month costs, how you're taxed, and whether your home has a role to play. I'll walk through the Ontario-specific parts with you, honestly.

No cost, no obligation, and I'm not a tax professional — just someone who can point you in the right direction.

The honest basics

The three government benefits most Ontario seniors rely on

These are federal programs — I don't administer them, but understanding how they fit together matters before you plan around anything else.

Old Age Security (OAS)

A monthly payment for Canadians 65 and older who meet residency requirements. You can delay starting it, up to age 70, in exchange for a permanently higher monthly amount.

Canada Pension Plan (CPP)

Based on what you contributed while working. You can start as early as 60 or as late as 70 — starting earlier means a smaller monthly amount for life, starting later means more.

Guaranteed Income Supplement (GIS)

An additional monthly benefit for lower-income OAS recipients. If you qualify, it's often applied automatically, but it's worth confirming with Service Canada directly.

The bigger picture

A retirement income plan usually has four legs

Most secure retirements I see aren't built on one source of money — they're a blend. Government benefits are only one leg of the stool.

- Government pensions: CPP, OAS, and GIS if you qualify.

- Personal savings: RRSPs and RRIFs, TFSAs, and any workplace pension you built up.

- Investment income: dividends, interest, or capital gains from non-registered accounts.

- Home equity: the value built up in your house, which can be accessed through a reverse mortgage, a HELOC, refinancing, or downsizing — if and when it makes sense.

That fourth leg is where I come in. It's not the first thing to lean on, and it's not right for everyone, but for homeowners who are equity-rich and cash-tight, it deserves an honest look rather than being ignored.

A practical exercise

Building an Ontario retirement budget

Skip the rule of thumb that says you need "70% of your working income." Track three real months of spending instead, then plan around these categories.

Housing

Mortgage or rent, property tax, maintenance, utilities, insurance. If your mortgage is paid off, this is often where the biggest change happens.

Healthcare

OHIP covers a lot, but not dental, vision, hearing aids, or most home care. Budget generously here — it tends to grow with age.

Daily living

Food, transportation, household items. Often lower than working years once commuting and work clothes disappear.

Travel & leisure

Hobbies, visits with family, the things retirement is actually for. Worth budgeting on purpose, not as an afterthought.

Family & giving

Helping kids or grandkids, gifts, charitable giving. Many of the families I talk to want to give while they're alive to see it help.

A cushion

An emergency fund for the unplanned — a roof repair, a health scare, a year the market is down. Retirement budgets without one tend to break.

Often misunderstood

How retirement income gets taxed in Ontario

Different sources of retirement money are treated very differently at tax time. Here's the general pattern — always confirm your own situation with a CPA or tax professional.

| Income source | Generally taxable? |

|---|---|

| CPP | Yes, taxable income |

| OAS | Yes, taxable income (may be partly clawed back at higher incomes) |

| GIS | Generally not taxable for the lowest-income recipients |

| RRSP / RRIF withdrawals | Yes, fully taxable as income |

| TFSA withdrawals | No, tax-free |

| Reverse mortgage proceeds | No — it's loan money, not income, so it isn't taxed |

Ontario also offers age-related credits — the age amount, the pension income credit, and medical expense credits that many seniors qualify for without realizing it. A tax professional who works with retirees can usually find a few hundred dollars a year that would otherwise go unclaimed.

Where I can help

How home equity fits into your retirement income plan

If your home is paid off or close to it, it's likely your single largest asset — and for many Ontario seniors, it's sitting there unused while the rest of the budget feels tight.

A reverse mortgage is one way to put that equity to work: no monthly payments, tax-free money, and you keep living in your home. It's not free money — interest accrues on the balance over time, and it reduces what's left for you or your family later. For some people a HELOC, a straightforward refinance, or downsizing is the better fit, and I'll say so plainly if that's what I see in your numbers.

The honest starting point is figuring out whether it belongs in your plan at all. Take the self-assessment or read the full picture on how reverse mortgages work.

Planning for care costs too?

Healthcare and home care are usually the biggest wildcard in a retirement budget. If that's on your mind, Home Care & Support walks through what care costs in Ontario and how families typically pay for it.