For Ontario homeowners 55+ and their families

Stay in the home you love. Use the equity you've earned.

I'm Ragini. I help Ontario seniors understand reverse mortgages in plain English, with no pressure and no jargon. Think of me as a trusted friend who happens to be a licensed mortgage agent.

A reverse mortgage lets homeowners 55+ turn part of their home's value into tax-free cash, with no monthly mortgage payments, while keeping full ownership of their home. It's right for some families and wrong for others. My job is to help you tell the difference.

No cost, no obligation, and no one will ever rush you.

The honest basics

What a reverse mortgage really is

It's a loan secured against your home, available to Canadian homeowners aged 55 and over. You can receive the money as a lump sum, monthly amounts, or both. Here's what makes it different from the mortgages you've had before:

No monthly payments

Nothing is due until you sell, move out permanently, or pass away. Interest is added to the balance over time instead of being paid monthly.

You keep ownership

Your name stays on title. The lender registers a mortgage, just like any other mortgage — the bank does not own your home.

You can't owe more than the home

Canada's reverse mortgage lenders guarantee that you'll never owe more than the fair market value of your home when it's sold, as long as you meet your obligations.

A different way to think about it

The "living inheritance"

Many families I meet aren't struggling — they're sitting on a paid-off home worth $800,000 while watching their kids fight a housing market that's nothing like the one they knew.

A reverse mortgage can let you give help while you're alive to see it: a down payment for a daughter, tuition for a grandchild, or simply taking the money worry out of your own retirement so your children never have to.

It's not about debt. It's about deciding what your home's value is for — and when.

Start wherever feels comfortable

Just researching?

Download the free plain-English guide — 20 pages covering how it works, honest pros and cons, costs, and the questions to ask anyone who wants your business.

Get the Free GuideWondering if it fits?

Work through a short, honest self-assessment. It will tell you when a reverse mortgage makes sense — and just as clearly when it doesn't.

Is It Right for You?Researching for a parent?

You're not intruding — you're being a good son or daughter. There's a page written just for you, including the protective questions you should ask.

For Adult ChildrenWho you'd be talking to

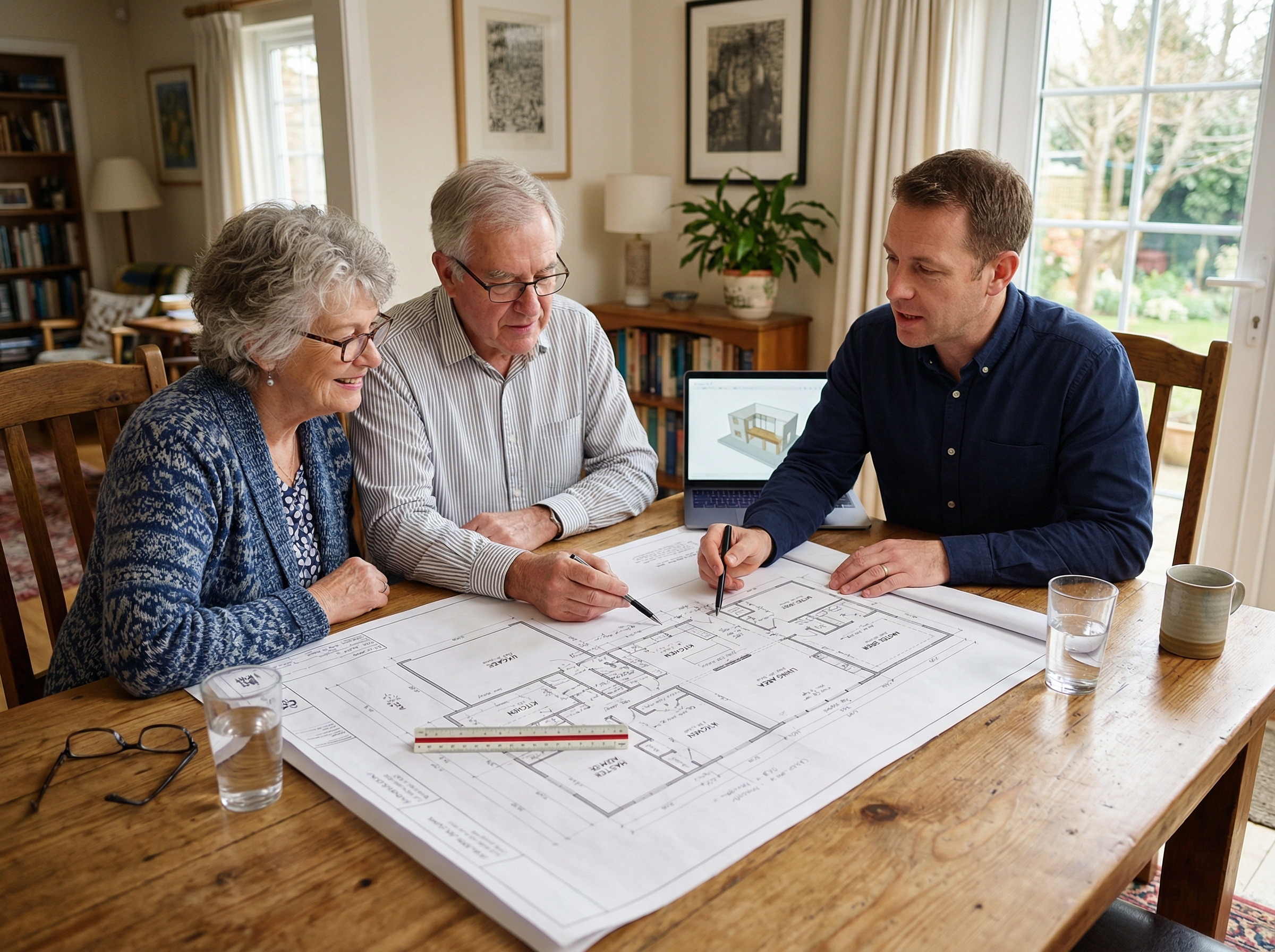

Meet Ragini Domenichini

Before becoming a mortgage agent, I spent more than 20 years in financial services compliance — at CIBC, BMO, Scotiabank, and OMERS. My whole career has been about making sure financial products are sold honestly and rules protect real people.

I bring that same instinct to this work: I'd rather talk you out of a reverse mortgage that doesn't fit than talk you into one that doesn't serve you. That's also why everything I do runs through a licensed brokerage, BRX Mortgage Inc. (FSRA #13549), and why I'll always encourage you to involve your family and get independent legal advice.

a real person, not a stock photo.

No-pressure promise

What happens when you call

- We talk for 15–30 minutes. You tell me about your home and what you're trying to solve. I'll tell you honestly whether a reverse mortgage could help — or whether something else fits better.

- You get numbers in writing. If it's worth exploring, I'll show you exactly what you could access, what it costs, and how the balance grows over time. Take it home. Show your kids. Sleep on it.

- You decide on your own schedule. Ontario lenders require independent legal advice before anything is signed — a lawyer of your choosing, working only for you. There is no step where you get rushed.

You're probably wondering

The questions everyone asks first

Can the bank take my home?

No. You remain the owner and stay on title. As long as you meet the loan's obligations — keeping the home as your principal residence, paying property taxes and insurance, and keeping it in reasonable repair — you cannot be forced out. The loan is only repaid when you sell, move out permanently, or pass away.

What happens when I die — will my kids inherit anything?

Your estate sells the home (or refinances), repays the loan balance, and keeps everything left over. Most borrowers still have meaningful equity remaining when the loan is repaid, because lending limits are conservative. The FAQ page walks through a full example with real numbers.

Is this one of those scams that target seniors?

Healthy question — keep asking it about everyone, including me. Reverse mortgages in Canada are offered by federally regulated banks and arranged through provincially licensed professionals. You can verify my brokerage, BRX Mortgage Inc. (FSRA #13549), on FSRA's public registry. Real scams pressure you to act fast; anyone rushing you is showing you who they are.

The Ontario Homeowner's Guide to Unlocking Home Equity Without Selling

A plain-English guide for homeowners 55+ and their families. Free, printable, and honest about the downsides too.

- How reverse mortgages actually work in Canada

- Reverse mortgage vs. HELOC vs. refinancing vs. downsizing

- Red flags that protect you from predatory offers

- A conversation guide for talking with your family

Send me the free guide

Let's talk, whenever you're ready

Questions? Just ask.

Whether you're curious about your own home or worried about a parent, I'm happy to answer questions with zero obligation. Call, or send a note and I'll reply within one business day.

Monday to Friday, 9am–5pm. If I'm with a family, leave a message and I'll call you back the same day.